Broker-dealer firms were once the backbone of advisor distribution and client service. They gave financial advisors the tools, products, and oversight needed to build practices.

But the industry has shifted. The rise of fiduciary-first, fee-based models has redefined what clients expect from their financial advisors. Investors now look for transparency, ongoing advice, and planning that goes beyond product sales.

So what is the value of broker-dealer business in a fee-first world? For many, the model feels outdated. For others, it remains a structure that provides compliance, scale, and resources that independent advisors still rely on.

The real question is whether broker-dealers are evolving fast enough to stay relevant. This article explores where BDs still create value, where they fall short, and what the changing landscape means for advisors choosing between the BD model and the independence of RIAs.

The Historical Value of the Broker-Dealer Mode

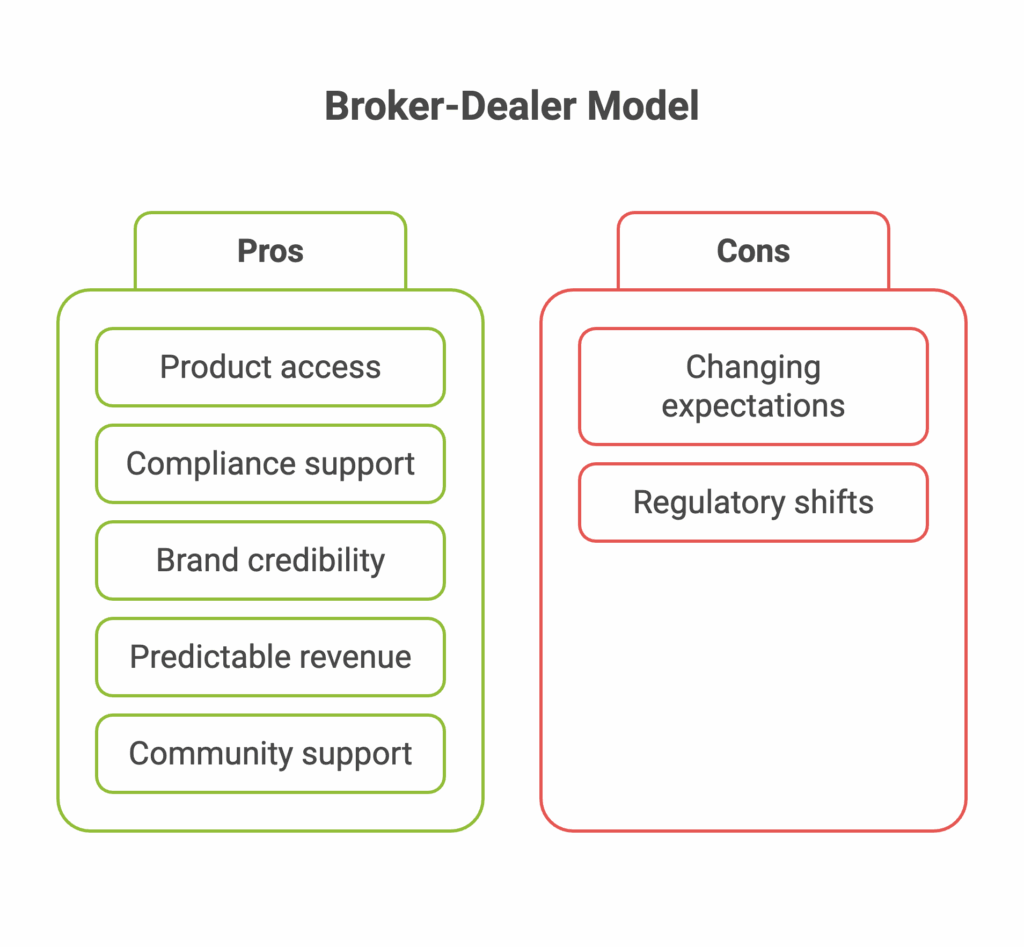

For decades, the broker-dealer model was the entry point for many financial advisors. The appeal was clear: access to products, compliance oversight, and the backing of a recognizable firm. For an early-career advisor, that combination provided credibility and a way to win clients before they had an established reputation of their own.

Product access was a defining advantage. Advisors could offer mutual funds, annuities, and insurance products through the broker-dealer’s shelf. In return, they received commissions, trails, and ongoing compensation streams. These payouts created predictable revenue for advisors and reinforced the business case for staying within the model.

The infrastructure also mattered. Broker-dealers carried the burden of compliance, trading operations, and risk management. Advisors could focus on sales and client relationships without worrying about the fine print of regulation or the mechanics of execution.

Beyond economics, there was an emotional draw. Many advisors tied their professional identity to the household name. A large firm provided the feeling of security and legitimacy. It meant they weren’t building alone. Conferences, recognition clubs, and advisor communities fostered a sense of belonging and reinforced loyalty to the system.

For years, the model was a winning formula. Advisors gained access, scale, and compensation. Broker-dealers thrived on transaction volume and product distribution. But shifts in client expectations and regulation began to change the calculus.

Why the Fee-First World Changes the Equation

The market has moved toward fee-based relationships at a rapid pace. Clients increasingly expect advisors to act as fiduciaries, putting their best interests first. This shift has redefined what advice looks like and how it should be paid for.

Regulation has accelerated the trend. The Department of Labor’s fiduciary rule and Regulation Best Interest (Reg BI) signaled a clear direction: less reliance on commission sales and more accountability for advice. Even though some rules were challenged or softened, the message to financial professionals was unmistakable (advice should be delivered in a way that minimizes conflicts).

At the same time, the registered investment advisor (RIA) channel has grown quickly. Independent advisors have embraced flat fee or percentage-of-assets models that emphasize transparency. Clients like knowing what they pay, without worrying if a transaction or product recommendation is influenced by compensation.

For advisors, the emotional dynamic is real. Many worry that clients perceive commissions as outdated or conflicted. A younger generation of investors, shaped by digital platforms and low-cost solutions, often prefers ongoing planning relationships rather than one-time sales.

The numbers back it up. A growing share of new client assets each year is flowing into fee-based accounts. This changes the revenue streams that once defined the broker-dealer model. Advisors who once relied on product sales now find themselves evaluating whether the structure still supports their long-term profitability.

The fee-first world has shifted the equation. What once seemed like stability in commission-based payouts now looks like a ceiling on growth. Advisors must ask whether the traditional broker-dealer structure aligns with client expectations, regulatory pressures, and the future of their practice.

The Value Broker-Dealers Still Provide

Despite the market’s move toward independence, broker-dealers continue to play a vital role for many advisors. Their value proposition now centers on infrastructure, scale, and support.

Compliance and risk management remain major draws. Navigating FINRA rules, Reg BI, and other oversight requirements consumes time and creates expense. Broker-dealers carry much of that weight, providing processes, audits, and supervision that give advisors peace of mind.

Access to capital is another advantage. Many broker-dealers provide loans or liquidity solutions to advisors who want to expand, acquire a book, or manage cash flow during transitions. For junior advisors or small practices, that access can mean the difference between stalled growth and a viable expansion plan.

Recruiting and training programs also matter. New advisors often need structure, education, and an entry point into the financial services profession. Broker-dealers offer this path, providing not only technical training but also a community of peers.

For senior advisors, transition support is critical. Broker-dealers often facilitate deals for retiring partners, connecting sellers with potential successors and managing the operational side of succession. These transitions tie closely to RIA succession planning, which helps advisors protect firm value and ensure clients experience continuity during ownership changes.

Technology has also become a point of value. Many broker-dealers now bundle portfolio management, trading systems, reporting platforms, and client portals into one package. This integrated approach reduces the burden of vetting multiple vendors and managing costs individually.

And then there’s the emotional comfort. For many advisors, being part of a larger firm provides stability. They don’t have to build operations, handle compliance, or take on every risk themselves. Clients, too, may feel more secure knowing their advisor is backed by a recognizable brand with established services.

In a fee-first world, broker-dealers must work harder to show value. Yet for advisors who want structure, scale, and support, the model still has real advantages.

The Limitations of Broker-Dealers in a Fee-First World

The broker-dealer model carries real strengths, but in today’s market, its limits are increasingly visible. The most common frustration advisors raise is payout compression. Independent RIAs often keep a larger share of their revenue, while broker-dealer reps give up a percentage of every account they manage. Over time, that difference can add up to hundreds of thousands of dollars in lost earnings.

Product restrictions are another sticking point. Many broker-dealers limit or control which mutual funds, annuities, or investment products an advisor can use. In some cases, marketing and client communication must be approved before distribution. Advisors report feeling like employees rather than business owners, despite being responsible for their own client base.

The compliance infrastructure that once felt like security can feel like a burden. Statistics show advisors expressing fatigue with layers of review, repetitive forms, and rules that seem designed more to protect the house than the client. Burnout is a recurring theme, with advisors saying they feel like “producers” rather than financial professionals trusted to deliver advice.

Clients are also changing. Fee transparency makes it easy for individuals to compare costs across firms. When clients see account fees and then hear about commissions or product payouts, some question whether the relationship is aligned with their best interests. That perception risks client attrition, even when advisors are acting in good faith.

The emotional undertone is clear. Advisors want to feel empowered, not constrained. They want to run a practice that reflects their values, not just the priorities of a broker-dealer. For many, the restrictions and bureaucracy have started to outweigh the benefits, pushing them to reconsider their long-term path.

When evaluating options, you also need to consider both internal and external succession planning for financial advisors. Internal succession offers continuity and cultural alignment, while external buyers often bring scale and capital. Both approaches highlight the trade-offs that mirror the broker-dealer vs. RIA decision itself.

Case Study – Broker Dealer to RIA Transition

One example comes from a mid-sized advisory team that decided to leave an independent broker-dealer to launch their own RIA. After years of frustration with restrictions on marketing and product access, they wanted more control over their firm’s direction.

The transition was not simple. In the first six months, they had to set up new compliance systems, migrate accounts, and reassure clients. Operations took more time than expected, and they absorbed costs for new technology and staff training. Some clients hesitated during the transition, uncertain about leaving the familiar brand behind.

But the long-term gains were clear. Their payout rose significantly, giving them more money to reinvest in client service. They expanded their offerings beyond traditional mutual funds to include new investment strategies and planning solutions. Most importantly, client trust improved. Without the shadow of commissions or firm-driven incentives, clients felt the advice was more transparent and personalized.

The lesson for other advisors: moving away from a broker-dealer can be challenging in the short term, but for many, the cultural alignment, control, and revenue growth outweigh the pain of the initial change.

Hybrid Models – The Best of Both Worlds?

Some advisors choose a middle ground: the hybrid model. In this setup, an advisor is dually registered, allowing them to operate as both an investment adviser and a broker. They can charge fees for planning and portfolio management while also earning commissions on certain products.

The appeal is flexibility. Advisors can serve clients who prefer fee-based accounts while still accessing commissionable products, such as insurance or certain mutual funds. For firms in transition, this model offers revenue diversity and helps avoid leaving money on the table.

But the hybrid model has tradeoffs. Compliance becomes more complex, as advisors must follow both RIA and broker-dealer rules. The messaging can also confuse clients. When one account is fee-based and another involves a commission on a sale, clients may wonder what drives the recommendation. Advisors must work harder to build trust and clearly explain the structure.

A hybrid model makes sense when an advisor’s client base has diverse needs and when commissions still play a meaningful role in delivering solutions. For others, the complexity outweighs the benefits. As the industry continues to shift toward greater fee transparency, hybrid models may serve as a bridge, but for many, they are not the ultimate destination.

How to Assess the True Value of a Broker-Dealer Relationship

Advisors weighing their options need a clear framework for evaluating the real value of staying with a broker-dealer. That assessment goes beyond revenue and payouts.

Economic factors come first. Payout rates, revenue share, and potential growth opportunities matter. Advisors should calculate not only current income but also long-term opportunity cost: what could earnings look like in an independent RIA structure versus remaining under the BD umbrella? For that reason, many advisors explore how to value a financial advisor’s book of business to better understand the trade-offs of staying with a BD compared to going independent. Knowing the true market value of a practice helps clarify the cost-benefit equation.

Operational factors include compliance oversight, staffing resources, and technology systems. Broker-dealers can reduce administrative time, but at the cost of flexibility. Advisors must ask if the systems are empowering growth or creating friction.

Emotional factors are often overlooked. Many advisors tie their professional identity to the broker-dealer that trained or supported them. The sense of belonging and perceived security can be valuable, but they may also keep advisors in structures that limit growth.

Client impact may be the most important factor. Clients increasingly demand transparency and fiduciary alignment. Advisors should consider how the BD model affects client retention, client experience, and overall trust.

When evaluating practice management and long-term succession planning, buyers of BD-affiliated practices often factor in compliance risks, payout variability, and client perceptions. A BD connection can add stability for some prospective buyers, but it can also reduce firm valuation if revenue streams appear less flexible.

The bottom line is that all advisors need to weigh the full cost-benefit equation. A broker-dealer may provide support and structure, but independence often delivers greater control and long-term profitability. The “value” of the BD relationship depends on alignment with both advisor goals and client expectations.

Future Outlook – Can Broker-Dealers Thrive in a Fee-First World?

The future of broker-dealers will likely hinge on consolidation, scale, and specialized positioning. Larger firms with the capital to invest in technology, client-facing platforms, and compliance support may maintain a strong role. Smaller broker-dealers without those advantages risk being acquired or fading out.

Adaptation is possible. Firms that pivot toward technology-driven operations, transparent compensation, and client-first cultures can still deliver meaningful value. Advisors who prefer structure, stability, and shared infrastructure will continue to see benefits from these firms.

But the broader trend is clear. Client demand for fiduciary, fee-first relationships grows each year, and independent RIAs are capturing a larger share of new assets. Broker-dealers that fail to evolve risk losing relevance.

Emotionally, the industry will remain divided. Some advisors feel empowered by independence, while others prefer the security of a large firm. The broker-dealer model won’t disappear, but its future role will likely be narrower and more specialized.

How buyAUM Supports Advisors Navigating the Choice

Deciding whether to remain with a broker-dealer, go independent, or pursue a hybrid model isn’t simple. buyAUM helps advisors assess the true value of their practice within the BD channel and beyond.

Our process begins with clarity. We provide accurate valuations, so advisors understand what their firm is worth today and how affiliation structures impact long-term value.

We also match advisors with buyers aligned to their philosophy, whether that means staying fee-first, exploring hybrid options, or finding partners who respect the BD framework. Every match is pre-screened to ensure cultural and strategic alignment.

Our services extend beyond valuation. We guide advisors through deal structuring, client retention strategies, and succession planning. We work alongside CPAs and attorneys to ensure transitions are tax-smart, compliant, and designed to protect client trust.

Start with your free TruValue Report.

Get a clear picture of your firm’s worth and explore the best path forward for your goals and your clients.

Redefining Value in a Changing World

Broker-dealers still provide value, but in a fee-first world, that value is shifting. Advisors must ask tough questions about alignment with client expectations, long-term profitability, and succession planning.

The right choice depends on your goals and your vision for the future. Independence, hybrid models, or staying with a BD can all work, but only with a plan that protects trust and maximizes value.

Begin with the TruValue Report.

Clarity is the first step to building a strategy that honors your legacy and positions your firm for what comes next.