Across the wealth management landscape, one trend is reshaping the industry: advisors splitting from big companies. More financial professionals are leaving wirehouses and national firms to strike out on their own, which often forms independent RIAs or joining fee-first platforms.

The shift is driven by a mix of opportunity and frustration. Advisors want more freedom to serve clients on their own terms, without the bureaucracy, payout grids, and product pushes that large firms impose. At the same time, clients are demanding transparency, flexibility, and fiduciary care, which are the standards that are easier to deliver outside of the wirehouse model.

But breaking away isn’t simple. Advisors face complex questions around compliance, technology, client retention, and capital. The rewards can be substantial, but so can the risks.

This article explores why advisors are making the leap, what they gain, what they give up, and how to navigate the decision with clarity and confidence.

Why Advisors Leave Big Companies

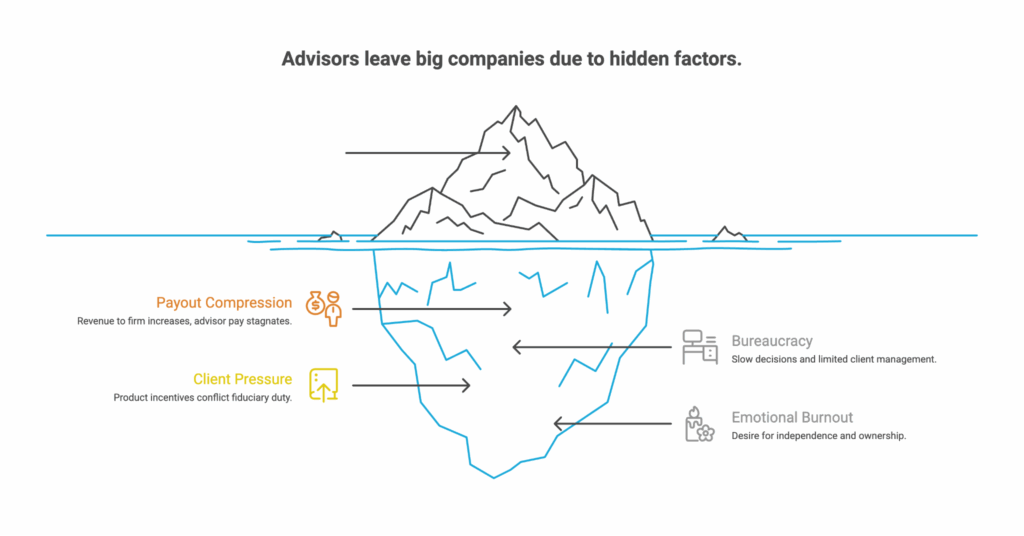

For years, large firms have attracted talent with recognizable brands, training programs, and a ready-made platform. Yet many advisors are walking away. The reasons are consistent across conversations.

First is payout compression. Advisors see more revenue going to the house while their compensation stagnates. The sense of being trapped inside grids or forced into cross-selling creates frustration. Bureaucracy adds another layer, which slows decisions and limits how client relationships are managed.

Client-facing pressure plays a major role. Advisors want to act as true fiduciaries, free to recommend solutions without worrying about product incentives. Working under a structure that prioritizes the distribution of a mutual fund or other packaged products can feel misaligned with the advisor’s mission.

Emotionally, many advisors reach a tipping point. They talk about burnout, a desire for independence, and the need to build something they truly own. As one advisor reflected, he felt reduced to a “producer,” not respected as a professional.

For some, this is the spark that leads them to look beyond the safety of a large firm. For others, it builds slowly until the opportunity for change becomes too clear to ignore.

The Psychological and Emotional Side of Breakaways

Going independent is more than a financial calculation. It’s an emotional crossroads.

Fear is real. Advisors worry about losing client assets in the transition. They worry about regulators, technology, and the unknowns of running a business. The idea of stepping away from the structure of a large firm can feel like standing on the edge of a cliff.

But hope is equally strong. Independence represents freedom. Advisors can finally design their practice, shape the client experience, and build equity. For many, it’s about leaving behind the identity of being a cog in a system and stepping into ownership.

This tug-of-war between fear and hope defines the breakaway journey. It’s all about identity, control, and legacy. And it explains why some advisors hesitate while others leap.

Operational Challenges Advisors Face When Breaking Away

The promise of independence comes with heavy operational demands.

Compliance is one of the first hurdles. Advisors must meet standards set by FINRA or register with the SEC, navigating an unfamiliar regulatory environment. It’s daunting without internal compliance support.

Technology is another challenge. Building a stack that includes CRM, trading, reporting, and client portals takes time and money. Large firms often provide these tools. Breakaways must now choose, integrate, and cover these costs themselves. –

The transition itself is disruptive. Advisors need to communicate proactively with clients, coordinate ACAT transfers, and reassure families about continuity. Staff transitions add complexity, as team members may or may not want to follow.

Cash flow is tight during the first year. Between legal costs, technology expenses, and lost time in transition, many advisors experience strain before the upside of independence arrives.

As one advisor said, “The hardest part isn’t finding clients like most think. It’s all about rebuilding the systems from scratch.” That sentence captures the hidden grind of a breakaway.

In this context, it’s important to plan for both short- and long-term outcomes, including future succession. Advisors preparing for this transition should also familiarize themselves with RIA succession planning strategies to ensure their long-term goals are protected from day one.

The Client Retention Question

Every breakaway advisor asks the same question, and that’s “will clients follow”?

Client retention often hinges on communication. Families want to know why their advisor is leaving and what it means for them. Silence breeds doubt, while proactive outreach builds trust.

In most cases, loyalty follows the advisor, not the firm. Clients value the person who has guided their financial planning and retirement decisions, not the logo on the statement. Still, reassurance is vital. Advisors must show that independence enhances, rather than disrupts, service.

Trust is the foundation. When handled carefully, client assets transfer smoothly. When handled poorly, attrition can erode both revenue and confidence.

A key part of this transition involves managing both client relationships and succession planning in tandem. Ensuring continuity for the client and long-term sustainability for the practice are equally essential.

The Strategic Upside of Going Independent

The upside of breaking away is compelling.

Independent advisors typically enjoy higher payouts and stronger margins long term. They control expenses and retain more of their revenue, instead of losing a portion to the house.

Ownership is another significant benefit. Advisors who leave a large firm and build their own practice are creating equity. The business becomes an asset that can be sold, transitioned, or passed on.

Understanding what your business is worth from the start is crucial. Learning about the average book of business for a financial advisor helps advisors benchmark their value and set realistic goals post-transition.

Independence also allows customization of the client experience. Advisors choose the technology, products, and services that fit their clients best, without restriction.

Finally, independence opens more opportunities for succession planning and partnerships. Advisors aren’t tied to the structures of large firms. They can sell, merge, or pass their practice on their own terms. For those exploring these paths, understanding the nuances of internal and external succession planning for financial advisors can make all the difference in long-term success.

Risks and Red Flags of Breakaways

Despite the benefits, risks remain.

Legal issues like non-solicits or non-competes can complicate client transitions. Some advisors underestimate these restrictions and end up facing disputes.

Transition costs are another red flag. Technology, compliance, and staffing expenses add up quickly. Without careful planning, cash shortages can become a serious problem.

Burnout risk is real. Independence means wearing every hat at first, and not every advisor thrives under that weight.

Finally, uncertainty takes a toll. If clients hesitate or regulators slow the process, momentum can stall. Advisors must prepare mentally for a challenging first year.

One way to reduce this risk is to plan your exit around value and timing. For those nearing a change, selling a financial advisory practice might be the right solution for realizing value without starting from scratch.

How buyAUM Helps Breakaways Find Their Footing

Breaking away doesn’t have to mean going it alone.

buyAUM helps advisors evaluate their options before making the leap. With expertise in practice management, valuation, and deal structuring, advisors can see clearly what their book of business is worth and how to protect it during transition.

Our process involves matching advisors with buyers or partners as needed, ensuring cultural alignment and client continuity. We also provide support on client retention strategies so assets transfer smoothly.

The first step is clarity. Start with your free TruValue Report to understand your firm’s value and build a roadmap for independence.

A Leap Toward Legacy

The breakaway movement reflects both risk and opportunity. Advisors splitting from big companies are making bold choices to claim independence, shape their legacy, and build practices on their own terms.

The journey requires clarity, preparation, and support. With the right guidance, the fear of leaving can transform into the freedom of ownership.

Your book of business is your future. Begin with the TruValue Report to make an informed, confident move toward independence.