When advisors think about selling or acquiring a practice, most of the attention goes to valuation and purchase price. Those numbers matter, but they don’t tell the whole story. The way a deal is taxed can change the outcome for both sides.

For a seller, the key issue is whether the proceeds qualify as capital gains or ordinary income. For a buyer, the question is how much of the purchase price can be deducted and when. These decisions ripple through cash flow, retirement planning, and even the long-term health of the firm.

That raises a central question: how do tax structures shape the real economics of an advisory firm deal?

This article breaks it down. We’ll cover the basics of how the IRS treats these sales, what buyers and sellers need to watch for, and the tradeoffs between different deal structures. We’ll also share strategies to reduce risk and highlight how the right planning can improve both financial outcomes and client continuity.

The Basics of Tax Treatment in Advisory Firm Sales

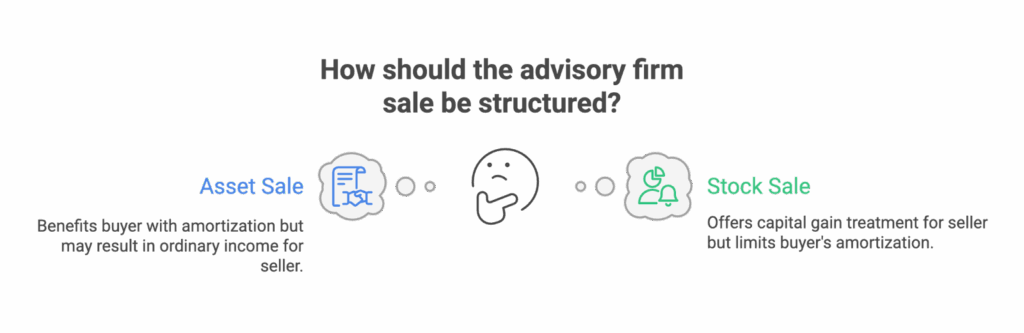

When a financial advisor sells a practice, the deal is usually structured in one of two ways: an asset sale or a stock sale.

In an asset sale, the buyer purchases the client relationships, goodwill, and sometimes tangible assets like office equipment. For tax purposes, this often benefits the buyer because the purchase price can be allocated to intangible assets and amortized over 15 years under IRS Section 197. For the seller, however, portions of the payout may be taxed as ordinary income rather than capital gain, depending on how the deal is structured.

In a stock sale, the buyer acquires ownership of the entire entity. This means taking on its contracts, client agreements, and potential liabilities. Sellers often prefer this structure because more of the proceeds may qualify for capital gain treatment, which usually results in a lower income tax rate. Buyers, on the other hand, lose the ability to amortize most of the purchase price.

What makes a financial advisory practice unique compared to other small businesses is the weight placed on client assets, recurring revenue, and goodwill. Unlike a retail company with inventory or real estate holdings, the financial advisor book of business is built almost entirely on trust and long-term financial planning relationships. That reality drives both the business valuation and the tax implications.

Understanding the value of those client relationships is key. If you’re unsure how to quantify it, here’s a guide on how to value a financial advisors book of business. Knowing the true worth of your book helps ensure the tax structure reflects actual market value.

Key Tax Considerations for Buyers

For a prospective buyer, the tax implications of purchasing a financial advisor’s book can shape cash flow for years. The most important advantage in an asset sale is the ability to amortize the purchase price over 15 years under IRS Section 197. This applies to goodwill, client lists, and other intangible assets. Each year, the buyer deducts part of the purchase price, which reduces taxable income and smooths the transition.

Another benefit is that recurring revenue from client acquisition is backed by tax-deductible costs. Unlike tangible assets, which may depreciate more quickly, intangible assets, such as client relationships, are spread out evenly across the amortization schedule. This stability helps with long-term financial planning and revenue projections.

Still, deal structure matters. If contracts, goodwill, and non-compete agreements are not clearly allocated in the purchase documents, the IRS could recharacterize payments. That might reduce the buyer’s deductions and raise income tax liability. For buyers financing the deal, unclear documentation can also complicate expense reporting and affect personal financial planning.

Cash flow is another key factor. Buyers who stretch to meet the purchase price may underestimate the lag before recurring revenue offsets debt payments. If amortization deductions are delayed or disallowed, the financial professional could find themselves in a shortfall.

The lesson for potential buyers is clear: structure and documentation matter as much as valuation. A well-written agreement ensures tax benefits are realized, while protecting the buyer’s future revenue stream and business worth.

Key Tax Considerations for Sellers

For the selling advisor, the biggest concern is how much of the payout will be taxed at favorable capital gain rates versus ordinary income tax rates. Payments allocated to goodwill and the financial advisors’ book often qualify as capital gains, which usually carry lower tax rates. Payments tied to consulting agreements or services, however, are taxed as ordinary income.

Non-compete agreements create another wrinkle. The IRS may view them as compensation rather than the sale of a financial advisory practice. That means higher income tax treatment for the seller. A selling advisor should ensure the agreement is fairly valued but not overly weighted in the contract.

Installment payments and earnouts also carry risks. While spreading payments out can help with personal finance and retirement planning, they can expose the seller to uncertain revenue if the buyer struggles with client retention. Earnouts tied to future revenue can create unpredictability in both income and tax reporting.

Understanding how other advisors navigate these challenges can offer a blueprint for success. If you’re in the early stages of planning your exit, this guide to selling a financial advisory practice lays out common pitfalls and how to avoid them, particularly from a tax and structural standpoint.

Common mistakes include underestimating the importance of allocations, failing to plan for income tax on short-term consulting payments, and not engaging a tax professional. These oversights can significantly reduce net proceeds from what looked like a strong business valuation on paper.

A successful transition for the seller means more than handing off client assets. It means structuring payments in a way that aligns with long-term financial goals and minimizes tax exposure. With careful planning, the sale of a financial planning practice can fund retirement while protecting years of client relationships and recurring revenue.

Comparing Asset Sales and Equity/Stock Sales

Most advisory firm transactions are structured as asset sales. Buyers prefer this model because they can select which assets they’re purchasing, avoid taking on hidden liabilities, and amortize the purchase price for tax purposes. For a financial advisor book, that often means allocating value to goodwill, client relationships, and other intangibles that can be deducted over 15 years.

Sellers may prefer equity or stock sales, especially in larger RIAs with multiple owners or complex structures. In these cases, the buyer acquires ownership of the entire entity, including contracts, staff, and sometimes real estate. From the seller’s perspective, equity sales often produce more favorable capital gain treatment, lowering the overall income tax burden.

The tradeoff is that buyers in equity transactions lose many of the tax benefits that come with amortization in an asset sale. They may also inherit compliance issues or liabilities tied to the firm’s history.

When navigating larger firm valuations, understanding market trends can be critical. To see how current market factors affect pricing, take a look at this breakdown of RIA valuation multiples. It highlights how structure and scale influence deal terms and potential tax strategies.

For smaller firms and solo practitioners, asset sales dominate. They provide clarity, cleaner tax benefits, and fewer surprises. For larger firms, equity deals can make sense if continuity of staff and structure is important, or if multiple retiring partners are involved.

Understanding these tradeoffs is critical for both the seller and the prospective buyer. The choice of structure can shift after-tax results by hundreds of thousands of dollars, making it a central part of the negotiation.

How Deal Structures Change Tax Outcomes

The way a transaction is structured can dramatically alter the tax bill for both parties.

Lump-sum buyouts provide immediate cash to the selling advisor, but also trigger an immediate tax event. If most of the purchase price is classified as goodwill, sellers may receive capital gains treatment. Buyers, however, take on a large debt load, which makes cash flow planning critical.

Installment sales spread payments over time. This approach softens the tax hit for sellers in some cases, since income is recognized as payments are received. The risk is that future payments depend on the buyer’s ability to maintain client retention and revenue. Buyers benefit from manageable cash flow, but interest paid on installments is taxable income to the seller.

Seller financing is common in the financial services industry. While it makes transactions possible when outside lending is limited, it shifts risk back onto the seller. The interest portion of payments is taxed as ordinary income, which reduces the net after-tax benefit for the retiring advisor.

Earnout structures are tied to future revenue performance. While they align buyer and seller incentives, they create tax uncertainty. Payments can be recharacterized by the IRS as ordinary income instead of capital gain, leaving the seller with a higher tax bill.

Two deals with identical valuations can result in very different outcomes once taxes are applied. A $5 million sale could leave one seller with $4 million after tax and another with closer to $3 million, depending on allocations, timing, and structure.

Strategies to Minimize Risk and Optimize Outcomes

Tax exposure doesn’t have to derail a financial advisory practice transition. With planning, advisors can protect value and create smoother outcomes.

The most important step is ensuring written agreements allocate the purchase price properly. Clear documentation that divides payments between goodwill, client relationships, and non-compete agreements prevents IRS reclassification and protects both sides.

Working with a valuation expert provides another layer of protection. A professional business valuation justifies allocations, supports compliance, and ensures the numbers reflect market reality. This is especially important when recurring revenue, client assets, and goodwill form the bulk of the financial advisor’s book.

Engaging CPAs, tax attorneys, and succession consultants early in the process is also key. Each plays a role in balancing the seller’s retirement planning needs with the buyer’s cash flow and amortization opportunities.

Finally, tax planning should connect directly to retirement planning goals. A structure that lowers taxes today but creates future income risk may not align with the seller’s long-term financial plan. Advisors who approach the deal with both business and personal financial planning in mind create more stability for themselves, their families, and their clients.

The bottom line is to treat tax planning as a core part of succession planning. Done right, it protects a business’s worth, secures client experience, and preserves more of the value built over decades.

Why Taxes Impact More Than Just the Deal

Every transition is also a moment that tests trust. Clients notice when their advisor is distracted, stressed, or consumed by details of a sale. If tax planning isn’t addressed, the advisor may walk away with less than expected, which can cast doubt on the entire process.

Taxes influence both the immediate payout and the long-term security of a retirement plan. A deal that looks strong on paper can leave far less in hand once income tax and reclassified payments are factored in.

Smart structuring reassures clients that the transition is stable, the business is prepared, and their financial planning relationship won’t be disrupted. Tax outcomes directly shape confidence for both the advisor stepping away and the clients who remain.

How buyAUM Helps Advisors Navigate Tax-Smart Transitions

Advisors don’t have to navigate these complexities alone. At buyAUM, we specialize in creating transitions that protect value while addressing tax considerations head-on.

Our process starts with valuation clarity. We deliver accurate, market-based insights into what your firm is worth, including the factors that buyers will evaluate when structuring the deal. From there, we help align purchase price allocations and structures in ways that balance valuation, tax treatment, and client retention.

We also pre-screen buyers to ensure cultural and philosophical alignment. The right buyer is prepared to maintain client trust and preserve the relationships that define your firm.

buyAUM collaborates with CPAs, tax attorneys, and succession consultants to craft tax-smart agreements. That coordination means fewer surprises and smoother execution, from the first offer through the final signature.

The best way to begin is with the TruValue Report. It’s a free first step to understand your valuation before building a tax strategy around it. With clarity on your numbers, you can plan with confidence.

The Real Value Is After-Tax

Every advisory firm transition comes down to more than price. The true measure of success is what remains after taxes.

For both buyers and sellers, tax-smart planning is crucial to protect value, enhance the client experience, and achieve long-term financial objectives. Deals that overlook this step often leave money on the table and create unnecessary stress.

The smartest path forward begins with clarity. Start with your free TruValue Report to understand your firm’s worth and explore strategies that keep more of your value intact. Your legacy deserves more than a valuation. It deserves a plan that works after-tax.