A Practical, Emotional, and Strategic Guide for Advisors Nearing Transition

For many advisors, their book of business isn’t just a spreadsheet.

It’s a career, a community, and a culmination of decades of trust. So when the time comes to ask, “how to value a financial advisors book of business?”, it’s not just about numbers.

It’s about LEGACY.

Valuation is part science, part emotion. Yes, there are metrics and multipliers, but there’s also meaning, what this business represents to you, to your family, and to your clients.

This guide isn’t theoretical. It’s built from hundreds of real conversations with financial advisors who are weighing tough choices:

Do I scale?

Do I sell?

Do I hand the reins to someone new?

They all want to do right by their clients, protect what they’ve built, and make smart, future-focused decisions. And that’s what we’ll help you do here, clearly, confidently, and on your terms.

The Advisor’s Inner Conflict – Beyond the Numbers

When most people hear the phrase business valuation, they picture spreadsheets, formulas, and neat little boxes to define what a financial advisory practice is worth. But if you’re a financial advisor, you know the truth: a valuation is rarely just about numbers.

It’s personal.

We’ve spoken to countless advisers, and what stands out is that few are primarily chasing a high multiple or the biggest revenue figure. Instead, they’re wrestling with questions like: Will my clients still be taken care of? Will the next person honor the values I built this on? Who will carry the torch when I step back?

This is the heart of the advisor’s inner conflict. You’ve built your client relationships over years, sometimes DECADES. You’ve offered financial planning, guided through life events, celebrated retirements, and consoled through losses. For many, this isn’t just an advisory firm

It’s a calling.

And that’s where the emotional weight hits hardest. When your identity is wrapped into your financial practice, even discussing a partner buyout or potential exit strategy can feel like abandoning a part of yourself.

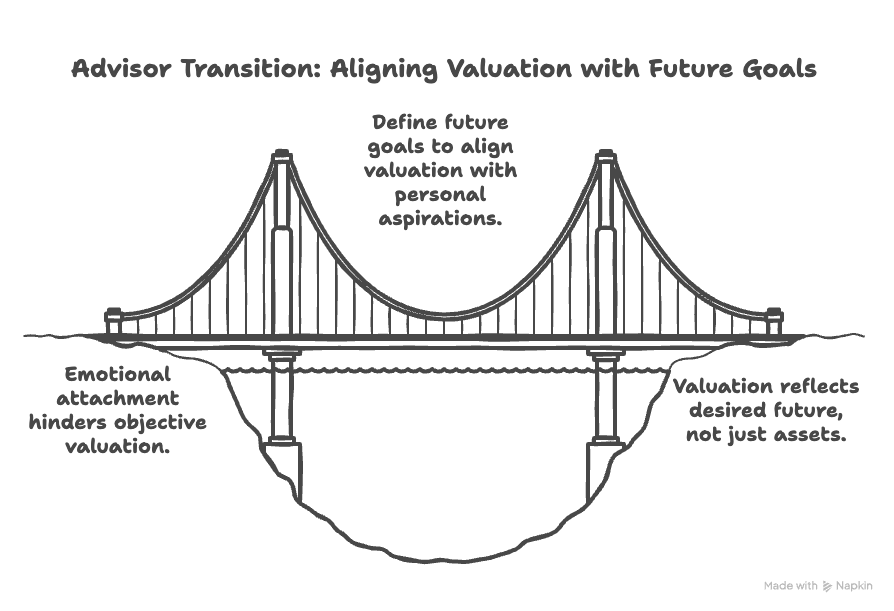

That’s why the smartest valuation method doesn’t start with EBITDA or discounted cash flow. It starts with one essential question: What future do you want?

Are you seeking more time with family? Space to pursue a new passion? The ability to scale your investment management business with a strategic partner? Each path requires a different approach, and your business worth should reflect those goals, not just your assets under management.

So let’s reframe the conversation. This isn’t about checking a box on practice management. This is about defining what a successful next chapter looks like for you, your team, and your existing clients. From there, we can reverse-engineer a valuation that’s both accurate and aligned.

Because ultimately, an objective assessment of your financial advisory book isn’t about where it’s been.

It’s about where it’s going.

The Core Valuation Frameworks Explained

If you’re a financial advisor preparing to assess your financial advisory practice, it’s essential to start with the right framework. Valuation isn’t a one-size-fits-all model. It’s a toolkit. And choosing the right tool depends on your size, your structure, and most importantly, your goals.

Let’s break down the three primary valuation approaches used across the financial advisory industry and often adapted for everything from solo investment advisors to multi-location wealth management firms.

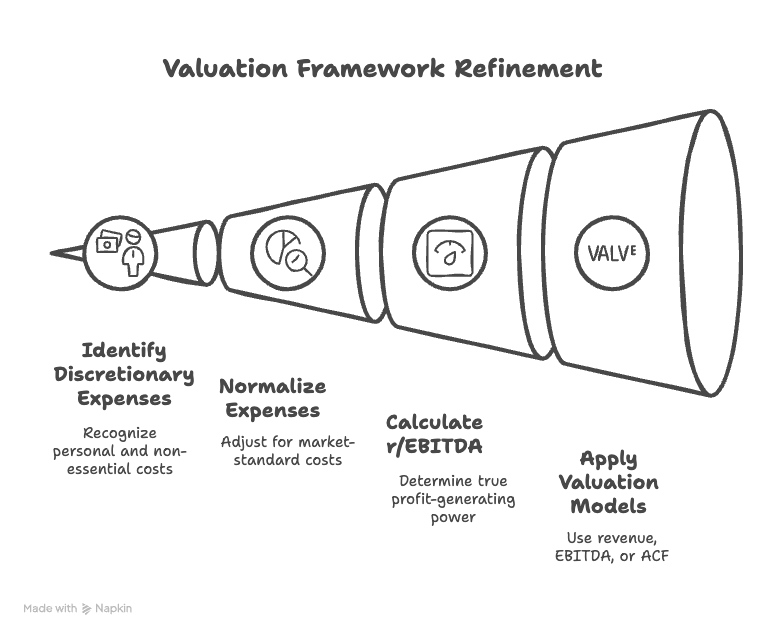

The Real Number vs. The Tax Number

Ask an advisor what their firm is worth, and you’ll often get their tax number, the net income that shows up on the books.

But buyers don’t base their offer on that number. They care about the real number: the true profit-generating power of the business when you strip out the owner’s personal lifestyle and normalize expenses.

Here’s how it works:

- If you pay yourself $1M/year but the market salary for your role is $300K, we add back $700K to get a more accurate earnings picture.

- Discretionary expenses, like car leases, travel, or family health plans, get backed out too.

- On the flip side, if you’ve underinvested in marketing or technology, we subtract what a buyer would reasonably need to spend.

The result?

A recasted EBITDA (r/EBITDA), a much more realistic picture of what a buyer is actually acquiring. This number becomes the foundation for nearly every serious acquisition conversation.

1. Revenue-Based Valuation

This is the most widely known and often quoted: a multiple of your gross revenue. It’s simple and quick, typically between 2x to 6x revenue.

For a more detailed breakdown of current trends and benchmarks, it’s worth reviewing updated insights on RIA valuation multiples. Understanding how these numbers are calculated and what drives them up or down helps you benchmark accurately and negotiate more confidently.

Also, it works best as a back-of-the-napkin estimate, especially useful in conversations with potential buyers or valuation experts. But remember, it doesn’t account for your cost structure, client demographics, or growth potential.

Advisors often lean on this model for its simplicity. But the danger is treating it as gospel. It’s a starting point, not a finish line.

2. EBITDA-Based Valuation

This model digs deeper, focusing on earnings before interest, taxes, depreciation, and amortization, essentially your profit engine.

It’s especially relevant for larger small business firms or multi-advisor teams where overhead and infrastructure play a significant role. If your advisory firm has strong margins, efficient client acquisition, and consistent operating income, this could yield a higher valuation.

EBITDA lets prospective buyers evaluate your firm like any operating company, comparing apples to apples with other financial professionals.

3. Adjusted Cash Flow (ACF) Approach

This is where things get personal and precise.

The ACF model adjusts for discretionary expenses and owner-specific costs to reflect the true earning potential of your business. It’s perfect for solo financial planners or practices where personal expenses and owner compensation can skew profit.

This approach often resonates most with advisors who want to provide a realistic snapshot of what a new owner, whether an internal successor or external partner, can actually take home.

Key Variables That Impact Value

Here are the levers that matter most, and the real reasons valuation experts look closely at them.

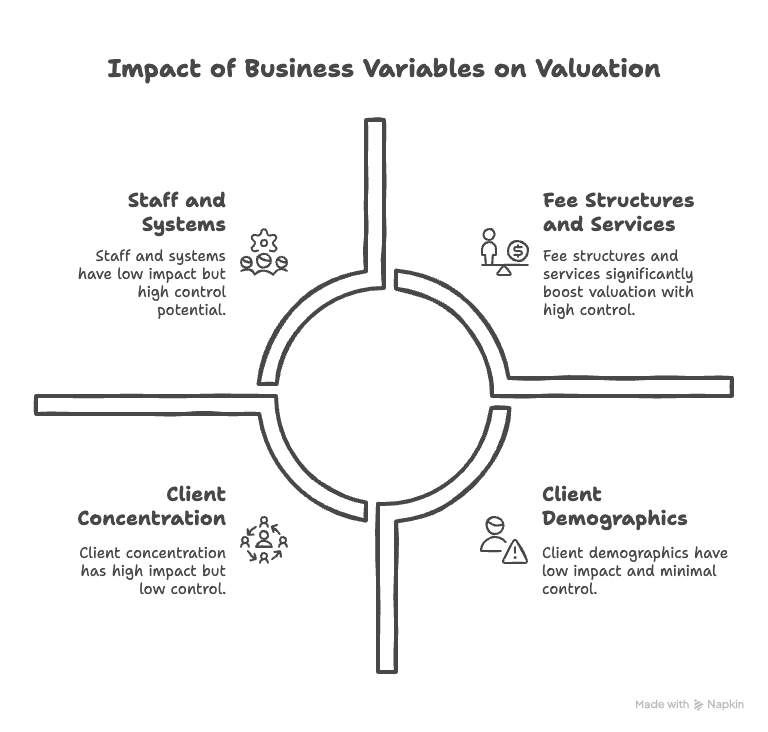

Client Demographics

Let’s say your book is mostly retirees. That’s great near-term revenue, but to a prospective buyer, it signals looming risk. Aging clients are less likely to grow their portfolios, and eventually, those assets may transition out through decumulation or estate transfers.

Sustainable value comes from client acquisition, not just retention. A balanced mix of new clients and legacy relationships paints a stronger long-term picture.

Client Concentration

If 50% of your AUM is tied up in your top three households, it’s not a business.

It’s a bet.

Client loyalty is important, but over-concentration is a red flag.

Many advisors didn’t realize this was such a big issue until they looked at it from the buyer’s perspective. Losing just one of those key assets post-sale can drastically alter the business.

Keeping your client concentration low is one of the clearest signals of a healthy, transferable financial advisory practice. While having your top three clients make up less than 30% of AUM is a common target, the gold standard is even more disciplined: no single client should account for more than 5% of your gross revenue.

This level of diversification significantly reduces perceived risk for prospective buyers and shows that your firm isn’t overly reliant on a handful of relationships. In turn, it boosts confidence in the sustainability of your revenue and the resilience of your business through a transition.

Fee Structures and Services

We’ve seen this over and over: advisors undercharging because they “don’t want to be pushy” or feel they “owe it to clients.” But here’s the hard truth. Undervaluing your services devalues your business.

Offering add-ons like financial planning, tax optimization, or even investment management models not only boosts income but also elevates the entire client experience.

One firm we worked with made a shift from charging 40 bps to a tiered structure that included financial planning, and saw its valuation increase by over 30%.

To the advisor, it felt like a bold move, rooted in concern about how existing clients might react. But to prospective buyers, it was a signal of a modernized, scalable revenue model.

That’s the emotional gap we often see: sellers think in terms of loyalty, relationships, and service history. Buyers, on the other hand, focus on structure, margins, and scalability. Bridging that gap often starts with small changes that make a big impact, all without compromising the trust you’ve built.

Staff and Systems

Founder-led is great until you want to leave. If your financial practice relies on one person to run everything from billing to meetings, the potential buyer sees risk, not value.

What buyers want is a team that runs smoothly without daily founder oversight. Strong operations, a clear service model, and repeatable systems show that your advisory firm is a business, not just a job.

The most valuable financial advisory practices aren’t necessarily the ones with the highest revenue. In fact, they’re the ones with the strongest foundation.

Advisors who invested in team development, technology, and operational workflows were building strength in their human, structural, customer, and social capital. These are the pillars that define a “best in class” business.

And in the eyes of prospective buyers, best in class doesn’t just earn respect but also a higher multiple. That’s the real win.

“Value Killers” That Sellers Often Overlook

You’ve spent years building your financial advisory practice. But when it comes time to assess its business valuation, there are often hidden pitfalls, things that quietly drag your value down without ever showing up on a spreadsheet.

Let’s call them what they are: value killers. And they’re more common than most financial professionals think.

Lack of a Succession Plan or Continuity Partner

One of the biggest deal-breakers for prospective buyers is uncertainty. If something happened to you tomorrow, who would step in?

A vague handshake deal or informal understanding doesn’t cut it. Continuity planning isn’t something you can scribble on the back of a napkin because it takes time to build trust, align values, and prepare both clients and successors for a seamless transition.

For those unsure where to begin, exploring dedicated resources on succession planning for financial advisors can be an excellent starting point. It provides a structured approach to building continuity and addresses both strategic and emotional components of a transition.

Here’s why it matters: 70% of widowed spouses change financial advisors after their partner dies, and a staggering 95% of children do the same after both parents pass away (Wojnor & Meek, 2011; Doolin et al., 2022). A poorly executed handoff means not just losing revenue, but losing generations of relationships.

Even the most loyal clients will start to look elsewhere if they sense a vacuum. And buyers? They aren’t just buying your book. They’re buying your plan. A clear continuity partner or roadmap is non-negotiable.

Emotional Resistance to Charging Appropriately

Many advisors undercharge because it “feels right” or they fear upsetting long-time clients. But here’s the reality: low fees can cost you far more in valuation than they save in client loyalty.

Buyers don’t just see underpricing. They see a perception problem. It signals that you may not believe in the full value of your service, and it creates an uphill battle to reset expectations with existing clients.

Think of it like wine. The same bottle sold for $5 or $50 will be experienced differently. People will savor the $50 version, recommend it to friends, and see it as exceptional, even if it’s identical. Why? Because perceived value is real value.

If you’ve been pricing your service like the $5 bottle, ask yourself: are you reinforcing loyalty, or quietly eroding it?

For buyers, pricing isn’t just about margins. It’s also about confidence in the offering. And if you want someone else to invest in your firm at a premium, you’ve got to show that you believe it’s worth it.

Philosophical Misalignment with Buyers

The best partnerships share values. But too often, deals fall apart not over money, but over mindset.

Are you a fiduciary, values-driven financial planner? Then selling to a high-volume, commission-oriented group could feel like betrayal, to you and your clients. We’ve heard this in many conversations: “They were offering a good deal, but it just didn’t feel right.”

Fit matters.

And helping advisers find culturally aligned partners often leads to smoother transitions and stronger outcomes.

Complacency: “I’m Doing Fine, So Why Change?”

This is the silent killer. You’re content. You’re profitable. Your existing clients love you.

But here’s the catch: life happens. Health changes. Family priorities shift. And without proactive planning, what was once a thriving advisory firm can suddenly become a fire sale.

We’ve spoken to investment advisors who waited too long, then had to settle for a fraction of what their financial advisor book was worth. Planning early is always about keeping your options open.

The Psychology of the Seller: What Really Matters

Dig beneath the surface of any financial advisor’s exit strategy, and you’ll often find something deeper than money driving the decisions.

Yes, revenue, cash flow, and multiples matter. But for many, the heart of the decision comes down to one quiet, persistent thought:

“I just want my clients to be okay.”

Case Study: The Advisor Who Didn’t Care About the Money

We spoke with one seasoned investment advisor whose practice was thriving, with steady growth, loyal clients, and no shortage of interested buyers. But when asked about price, his answer was simple:

“I don’t need the money. I just want someone who will do right by my clients.”

For him, legacy wasn’t about maximizing his business valuation. It was about making sure the values he built the firm on, which included honesty, simplicity, and long-term relationships, lived on after he stepped away.

This isn’t a rare sentiment. In fact, it’s a pattern we see often.

When Monetization Becomes Secondary

Many advisors delay serious conversations about valuation because they don’t see it as urgent. They’re “not ready,” “still love the work,” or “have time.”

But then something shifts. A new grandchild is born, a spouse retires, or a health scare happens. Suddenly, the conversation isn’t about valuation methods or potential buyers but about time. And impact. And peace of mind.

It’s about knowing that your client relationships, your financial goals, and your firm’s future are protected.

And at that point, even the most numbers-driven seller will tell you: it’s not about extracting every last dollar from the deal. It’s about ensuring continuity, care, and a philosophy match that honors what they’ve built.

Increasing the Value of Your Practice (Without Selling Out)

You don’t have to sell your soul, or your style to increase your firm’s value. The real lever is increasing your multiple. And the way to do that? Strengthen your core business capital: human, structural, customer, and social. These Four Cs account for as much as 80% of a firm’s business valuation.

The goal is to move from below average, to above average, and eventually to best-in-class. That’s when buyers take notice, and when your practice commands a premium.

Charge What You’re Worth

This one hits hard. We’ve heard from countless advisors: “I don’t want to rock the boat.” But undercharging, especially after years of client loyalty and trust, can undercut your entire valuation.

Revisiting your fee structure isn’t about being greedy. It’s about matching the value you deliver. And guess what? When you position it well, existing clients often get it. Especially if you tie it to expanded services and client experience upgrades.

Introduce Planning and Tax Services

If you’re not offering financial planning or tax strategy, you’re leaving value on the table. These services increase revenue, deepen client relationships, and offer more touchpoints that make clients stick.

Buyers see these as growth levers, especially if they’re not tied to a specific person (see next point).

Reduce Founder-Dependence

Is everything in your head? Then you’ve got a job, not a business.

Systems, repeatable processes, and delegation don’t just make life easier but also make your practice transferable.

Transferability isn’t just a value booster. It’s everything. If your business can’t run without you, it’s not a business. It’s a job. And buyers don’t want to buy a job. They want recurring revenue and reliable returns.

Benchmark with a “TruValue Report”

Sometimes you just need a starting point. Our TruValue Report gives you a quick, high-level snapshot of your financial advisor book’s worth, based on real-world market inputs. It highlights strengths, identifies gaps, and points to easy wins, without pressure or commitment.

You can’t fix what you don’t measure. And this tool gives you a smart, efficient way to do just that.

Strategic Exit Options and Their Impact on Valuation

There’s no one way to transition your advisory firm. Each path comes with its own set of risks, rewards, and emotional hurdles. Here’s a look at the most common routes, backed by what we’ve learned from real advisor stories.

Full Sale

This is the clean break. You sell 100% of your firm, walk away (gradually or immediately), and hand over the reins.

Pros: Maximum liquidity, simplified exit, full off-ramp.

Cons: Loss of control, potential mismatch with new owner’s values, emotional weight of “letting go.”

Understanding the nuances of selling a financial advisory practice is critical before making this leap. From deal structure to client retention strategies, having the right framework can mean the difference between a smooth exit and a valuation shortfall. A clear strategy helps align both financial outcomes and legacy goals.

Minority Stake Sale

Think of this as scaling with a seat at the table. Groups like Apollon or Little House offer infrastructure, back-office, and growth support in exchange for equity.

Pros: Leverage scale without selling out, stay involved, boost revenue, and capacity.

Cons: Need to align on vision, partner selection is crucial.

This path has gained traction among wealth management firms that are already performing at an above-average or best-in-class level, but have a generational challenge. Often, older partners are ready to transition out, while younger partners don’t have the capital to buy them out at fair market value.

A minority stake sale, typically involving private equity or a scaled platform partner, offers a solution. It brings in the capital, infrastructure, and strategic support needed to move the firm to the next level, without compromising independence or culture.

Internal Succession

Pass the baton to a junior advisor or family member already in the business.

Pros: Cultural continuity, trusted relationships, deep understanding of the client base.

Cons: Often lower upfront payout, requires a long runway to prepare the successor, and emotions can run high.

From the Field: Advisor Reflections

We’ve talked to those who sold too soon. Others who waited too long. And many who found the sweet spot in the middle and partnered with platforms that respected their legacy while fueling the next phase.

Whatever route you choose, clarity matters. And so does alignment with your goals, your clients, and your future self.

Conclusion

You’re not just selling a book of business.

You’re passing a torch to someone who will carry on the relationships, values, and impact you’ve built.

And that makes this moment bigger than a multiple or a spreadsheet.

True valuation isn’t just financial. It’s relational. It’s emotional. It’s a reflection of your life’s work, and a setup for what comes next.

Exit planning is simply a good business strategy. It strengthens your operations, aligns your team, and makes you more attractive to prospective buyers, regardless of whether you plan to sell next year or in ten.

Exit planning should be present tense. Not a future to-do, but a current mindset. Because when you understand your worth today, you gain leverage, clarity, and options for tomorrow.

So whether you’re years from retiring or just starting to think about it, don’t wait. Start with a conversation. A valuation. A fresh look at your future.

Because when it comes to your financial practice, it’s not about when you sell but about being ready when the time is right.

Let’s help you get there with clarity, confidence, and care.

Get your free TruValue Report now.